3 Days Down Overnight Trading Strategy (S&P 500, Nasdaq, Rules, Performance, Video)

Here is a simple mean reversion twist in SPY that holds the S&P 500 just one day (from the close to the next day’s open or close). It’s an overnight trading strategy, the lowest-hanging fruit in the stock market (?).

This article was initially published in 2013, and it’s about time we updated it. We thus have plenty of out-of-sample data.

- Three 24-Hour Day Trading Strategies (strategy bundle)

The 3-day down overnight trading strategy

In plain English, the trading rules of the strategy reads like this:

Trading Rules

[am4show have=’p2;p3;p58;p59;p130;p138;’ user_error=’Premium Post Access’ guest_error=’Premium Posts’]

- SPY must be down three days in a row (from close to close).

- Entry on close on the 3rd down day.

- Exit the next day open.

[/am4show]

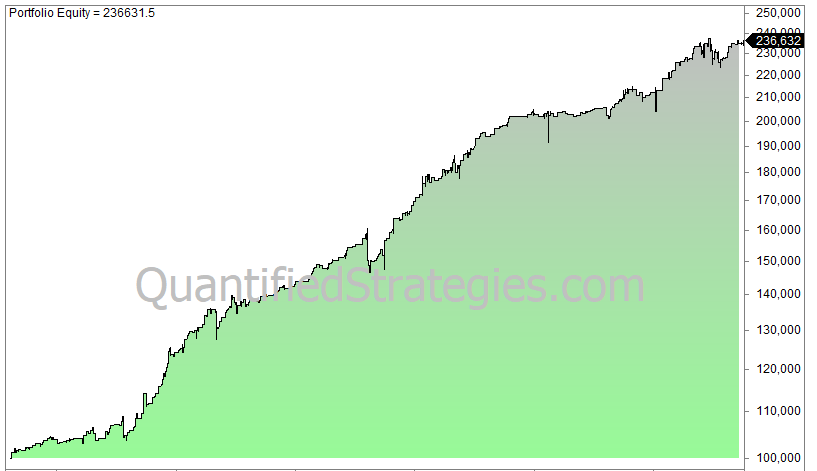

Here is the equity curve from 1993 for SPY, which tracks S&P 500, until today (backtest done in Amibroker):

There are 661 trades, and the average gain per trade is 0.13%. This might not sound much, but in a liquid asset like SPY, this might be tradeable even though slippage and commissions are not included in the backtest. Please read our article about realistic slippage and commissions for liquid ETFs.

The win rate is 65%, and max drawdown is 8%.

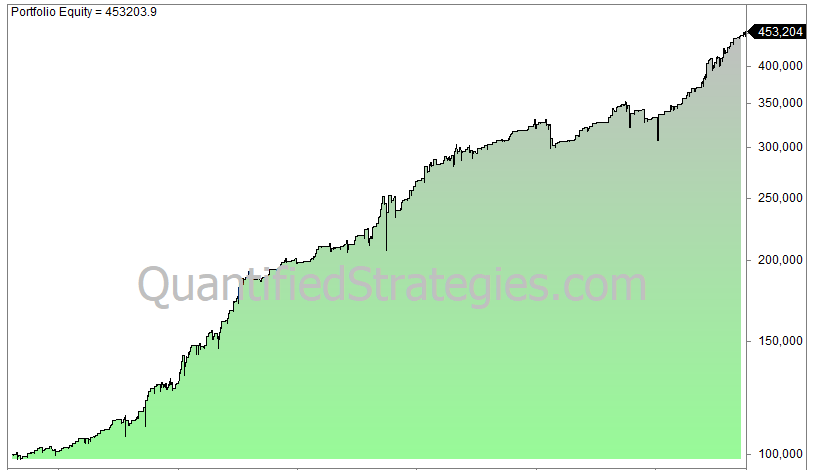

Let’s change the rules and exit on the close instead of the open:

Exiting on the close the next day is even better: the average gain increases to 0.24%.

The drawback is that the win rate drops to 61%, and max drawdown increases substantially to 17%. The CAGR is 5% despite spending just 8% of the time in the market.

The strategy also works for Nasdaq 100 (QQQ) and many stocks, but not as well as for S&P 500.

Can the strategy be further improved?

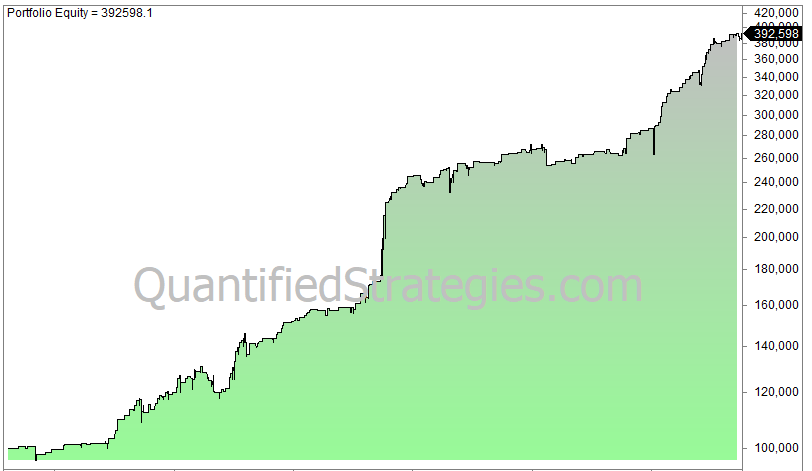

Yes, in our Monthly Trading Edge for March 2022, we made a modified version of the strategy above that returned the following equity curve (less time in the market and smaller drawdowns):

- No. of trades: 419

- Average gain per trade: 0.35% (1.35% for winners and -1.15% for losers)

- Win ratio: 60%

- Profit factor: 1.78

- CAGR: 4.5% (assuming no leverage)

- Exposure/time in the market: 5%

- Risk-adjusted return: 84% (CAGR divided by time spent in the market which is 0.05)

- Max. drawdown: -10%

In the bear market of 2022 (out of sample), the strategy made 35 trades and the average gain was 0.3%.

The last strategy is one of 3 strategies that are part of the Three 24-Hour Day Trading Strategies Bundle.

—————————

If you would like to have the code for this strategy plus 200+ other trading strategy types published on this website, please click on this link:

For more trading strategies, please click here:

- Monthly trading edges (subscription service)

Is there a reason most of your strategies are on ETFs? Do you not trade anything on individual stocks?

Hi,

Yes I trade individual stocks more than ETFs. But I’m afraid to lose my edge if I publish it.

Hi Oddmund,

Could you explain more in detail what the three steps of this strategy are please?

What are the horizontal and vertical lines of the graphs are?

Thanks

The y-axis are accumulated %. The x-axis is #days in the test.

Hi Oddmund,

I have seen you backtesting swing/overnight strategy on SPY that has historically < 200 trades. Do you think this is statistically significant enough?

I believe you have executed some of them and could probably tell whether this is real edge or not.

Hi, probably not statistically significant, but taking advantage of the risk premium.

Hi Oddmund,

I’m trade similar strategy on individual stocks. Go long after 2 red day candles on MOC and cover on MOO.

Hi, for how long have you traded this strategy?

Hi Oddmund,

An American friend advised me to check out your page. I am amazed to find out that you are Norwegian like me 🙂 It just proves the international scope of trading I guess.

I have a question regarding the 3dayDown strategy above. How would you put this i operation? Use minute data and for example, 30 min before close, as your closing price for the day-end? Another question, which broker and API do you use?

Looking foreward to your next post,

Best regards Snorre

Yes, I’m Norwegian 🙂

This strategy I just buy SPY some seconds before the close.

I’m using IB and their API (I use Excel for sending orders).

Oddmund

Hi Oddmund,

can you explain whats the way the put the MOC order since MOC order have to be put 15 minutes before you know if you are in the 3rd down day ¿¿??

Best regards

Alex

Hi Alex,

You simply have to put in an order just seconds from the close. But with SPY you cal always enter after market close because it’s so liquid.