One Peculiar Pattern in GDX (Gold Miners) – Is It Good Enough to Trade? Insights and Analysis

Let’s look at an interesting and peculiar pattern in GDX – gold miners:

We have in many articles mentioned the tailwind from the overnight edge.

We use the following trading rules:

[am4show have=’p2;p3;p58;p59;p130;p138;’ user_error=’Premium Post Access’ guest_error=’Premium Posts’]

- We enter long at the close on every trading day;

- We sell at the open the next day.

[/am4show]

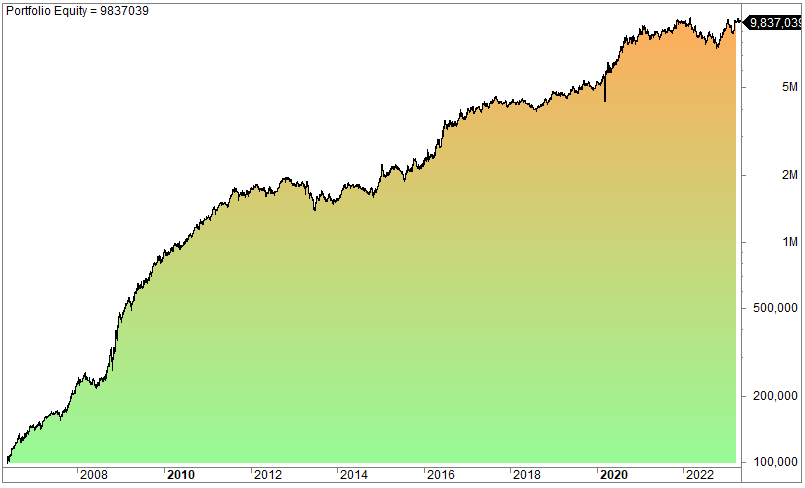

This strategy has returned the following equity curve:

The average gain per trade is 0.12%, and it’s not tradable as it is.

But GDX has a second interesting pattern/bias:

[am4show have=’p2;p3;p58;p59;p130;p138;’ user_error=’Premium Post Access’ guest_error=’Premium Posts’]

- We short the open every day, and;

- We cover the position at the close the same day.

Amibroker code for both strategies:

Buy = C>0 ; buyPrice=Close;

Sell = C>0 ;//forced "no exit"

SellPrice = Open;

applyStop(stopTypeNBar,stopModeBars,1,1);

short= C>0;

shortPrice= Open;

Cover= c>0; //force exit

coverPrice= C ;[/am4show]

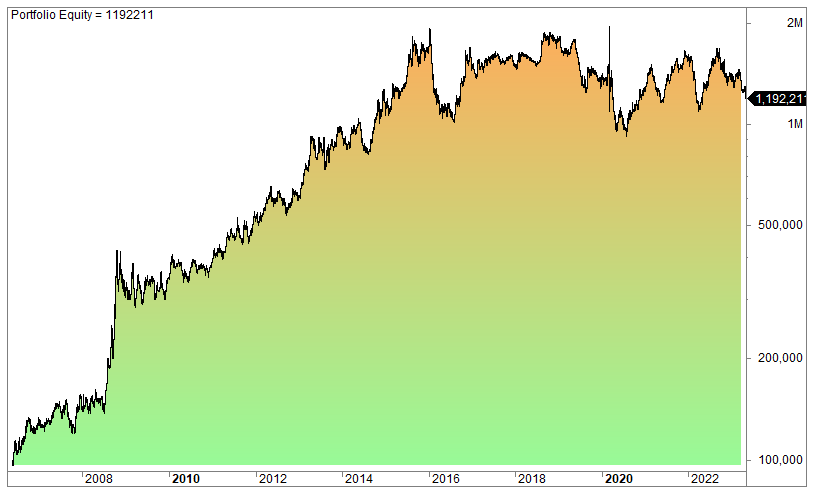

This is the equity curve:

The performance over the last few years has been mediocre, but the bias is clear: negative. The average gain has been 0.08%.

Obviously, none of this is tradable as is. However, we have some exciting trading rules for incubation and might publish them later if they survive our 12-month test period.

Disclaimer

Quantified Strategies (SIA Lofjord) is not an investment advisor. The content and information provided are educational and should not be treated as financial advisory services or investment advice. Trading and investment in securities involve substantial risk of loss and is not recommended for anyone that is not a trained trader or investor – it shall be conducted at your own risk. It is recommended that you never risk more than you are willing to lose. Leverage can lead to substantial losses. Any use of leverage, margin, or shorting is at your discretion. Quantified Strategies (SIA Lofjord) is not responsible for any losses that occur as a result of its content and information.

Hypothetical or simulated performance results have certain limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, Since the trades have not been executed, the results may have under or overcompensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs, in general, are also subject to the fact that they are designed with the benefit of hindsight. No representations are made that any account will or is likely to achieve profit or losses similar to those shown.

FAQ:

What is the overnight edge in GDX trading?

The overnight edge in GDX trading refers to a pattern where trades are initiated at the close of each trading day and closed at the open of the next day. This strategy is explored to capture potential gains from overnight movements.

Is the GDX overnight edge strategy immediately tradable?

The rules involve entering long at the close of each trading day and selling at the open the next day. The Amibroker code is provided for implementing this strategy. The strategy, as presented, is not immediately tradable due to a low average gain per trade (0.12%). However, the content hints at ongoing analysis and potential modifications to make it viable.

What is the alternative bias observed in GDX trading?

The performance of the short bias strategy has been mediocre in recent years, with an average gain of 0.08%. However, the clear negative bias is highlighted. The article discusses a second pattern/bias in GDX trading, where short positions are initiated at the open and covered at the close of the same day. The equity curve and performance metrics are provided for this strategy.